In May 2018, eight months after he fully exited Flipkart following Walmart’s $16 billion acquisition of the e-commerce firm, Bansal launched his second venture. This time, Bansal waded into the booming world of fintech with Navi Technologies, focusing primarily on lending, and later, to a lesser extent, on insurance and investments. Navi also started Unified Payments Interface (UPI) services in August 2023, a space heavily dominated by PhonePe and Google Pay. It has racked up users swiftly, but has a long way to go.

“When we started, we saw two extremes in the fintech space,” Bansal told Mint during an interview at Navi’s office in Bengaluru earlier this month. “One: traditional players who take risks on their books but outsource tech. Two: fintechs that build great tech but don’t take any financial risk themselves.”

For Bansal, the answer lies in doing both: building proprietary technology and underwriting risk in-house, betting that this end-to-end approach will set Navi apart in a crowded market. “In India, you can’t just be a layer. You have to solve the whole problem,” he said. “And that was one of the learnings that I had at Flipkart.”

Bansal’s ambition has been a costly affair. He owns more than 90% of the company; and has invested close to $500 million of his own funds in Navi. “We’re not burning too much cash overall at a group level. But we do need capital to grow our lending book,” he said.

We’re not burning too much cash overall. But we do need capital to grow our lending book.

—Sachin Bansal

To raise money, Navi, last valued at $500 million, is eyeing a long-delayed IPO again in the next 12-18 months. However, the volatility in the market seems to be dampening this plan. Meanwhile, behind closed doors, scepticism is brewing. Those with direct knowledge of Navi’s operations say that with Bansal’s massive ambition, the company has so far struggled to carve a clear edge, and its financials haven’t firmed up.

Aside from regulatory clampdowns, including a short ban on lending, Navi has been hit by multiple roadblocks. A string of top-level exits has also eroded its credibility. As the fintech boom cools and scrutiny tightens, Navi finds itself at a critical juncture.

Given all these challenges, can Bansal script a second act as iconic as his first? Industry insiders are not convinced he can. Indeed, they believe Navi’s reported $2 billion valuation ambition is far removed from reality.

While some media reports have indicated that the company is looking at private funding, Bansal denied any such plan. He didn’t disclose the valuation the IPO would target.

Why fintech?

Bansal’s decision to launch Navi as a full-stack tech-led financial services platform wasn’t taken overnight. As early as 2016–17, Flipkart had been eyeing financial services as its future profit engine. “The board (including Bansal) realized lending had the deepest profit pools, and had started scaling fintech efforts seriously,” said a former Flipkart executive who didn’t want to be identified. However, post the Walmart acquisition, financial services, seen as non-core to Walmart’s vision, took a backseat.

View Full Image

Navi allowed Bansal to keep this fintech vision alive. When the startup launched in 2018, according to a KPMG report that year, total investment in fintech across the globe had more than doubled from $50.8 billion in 2017 to $111.8 billion, with payments and lending leading the way.

In India, too, fintech saw a sharp upswing, with around $2.45 billion invested, especially after the launch of UPI and cheaper data from Reliance Jio. This was also the time when Paytm raised $356 million and PolicyBazaar closed a $200 million round.

Bansal’s early strategy was clear: build a lending engine first, then broaden into financial services. Navi started with short-term unsecured personal loans and diversified into longer-tenure home loans in 2020. Together, the two heads make up about 70% of the business.

From underwriting and data science models to apps, websites, risk systems, and collections, everything was built in-house. This internal control allowed Navi to move faster, Bansal said.

When regulations suddenly changed to mandate concurrent audits for video KYC, Navi launched the updated process within days—without disrupting the user experience. “The differentiation lies in how the service feels to the user. It’s the sum of all these seemingly small efforts—some big, some subtle—that ultimately sets us apart,” he said.

Bansal also made a conscious choice to avoid hiring traditional banking talent. “The pros of having fresh talent brought into the space, and giving them the same problem set, is that they think from first principles. There’s no other option for them,” he added.

In 2019, Navi acquired Chaitanya Rural Intermediation Development Services Pvt. Ltd (CRIDS) to establish a stronger foothold in the lending segment. This was followed by a spree of acquisitions: technology consultancy MavenHive (2019) to bolster in-house tech capabilities, Essel Mutual Fund (2020) to launch Navi AMC, and DHFL General Insurance (2020) to enter the insurance sector.

With these moves, Navi stitched together a full-stack portfolio across loans, investments, and insurance. “Our core focus continues to be on credit. But we know that in the future, we will not just stick to that,” said Bansal.

Navi filed for an IPO in March 2022, aiming to raise ₹3,350 crore. According to its DRHP, the company planned to invest a large chunk of capital into the growth of its lending business, while the remainder would go into the insurance business.

Alongside, in its DRHP, Navi revealed its plans to secure a universal banking license through its subsidiary Chaitanya India Fin Credit—a move that would have fundamentally reshaped its trajectory. For Bansal, the banking licence was the ultimate piece of his neobanking aspiration.

However, just when Navi’s lending ambitions had started to soar, the regulator cracked the whip.

Setbacks aplenty

In May 2022, the Reserve Bank of India (RBI) rejected the banking licence application amid concerns over Bansal’s legal woes—tied to Fema irregularities during his Flipkart days and matters on the family front—and compliance lapses in customer data handling at Navi Group.

View Full Image

Navi has now paused its banking aspirations. “We have to see whether the regulator is open to giving out new licences,” said Bansal. This comes despite one of its peers, Slice, receiving approval from the RBI to merge with Guwahati-based North East Small Finance Bank Ltd, effectively winning a banking licence.

Eventually Navi ended up selling CIFCPL to Ananya Birla-led Svatantra Microfin in a deal valued at ₹1,479 crore in August 2023.

The IPO ambitions, too, were put on hold soon after. “The Ukraine war started and all the tech stocks were down. So, we said we’ll pick it up some other day,” said Bansal.

Now Bansal plans to go public in the next 12 to 18 months, and refile a DRHP by March 2026. Volatility in the markets, driven by global tariff wars and rising regional tensions, has made high pre-IPO valuations debatable. Recent fintech IPOs, such as PBFintech and MobiKwik, have seen sharp corrections from their January highs, showing concerns around valuations and IPO timings.

Separately, the RBI’s tight grip on the fintech sector over the past few years has weighed heavily on Navi and others in the space. The digital lending guidelines of 2022 mandated stricter disclosures and curtailed practices such as first-loss default guarantees (FLDG).

The unregulated fintech industry often partnered with regulated entities to pass on customer leads and banked heavily on the FLDG arrangement to make a loan happen. In such an arrangement, the fintech compensated the regulated entity in case a borrower defaulted.

In November 2023, the RBI further directed banks and NBFCs to provision more capital against unsecured loans and moderate their exposure to riskier retail segments.

Bansal plans to go public in the next 12 to 18 months. However, volatility in the markets, driven by global tariff wars and rising regional tensions, has made high pre-IPO valuations debatable.

Hit by the crackdown, fintech lenders spent most of 2024 cleaning up their books, cutting back on risky loan portfolios, and pivoting toward co-lending and secured loan products such as home loans. Navi, which had relied heavily on unsecured loans, has also seen its secured loans segment grow.

“It’s not that I was unaware that this would be a regulated space. But I definitely think that there has been a change of environment from a regulations perspective. They have become stricter than before,” said Bansal. “If you (the regulator) cut risk, you also cut upside.”

For Navi, that has resulted in an alteration in its loan book. Bansal confirmed to Mint that personal lending will gross up to about 85% of the lending book in FY26, down from 90%, while the home loan segment is expected to grow, without sharing details.

The turbulence deepened in FY25, when the RBI barred Navi, along with three other NBFCs, from lending and disbursing loans over violations related to pricing policies and compliance norms. “In hindsight, yes, we should have charged lower interest rates. But…you have to judge that without having clear guidelines. That’s the challenge,” said Bansal.

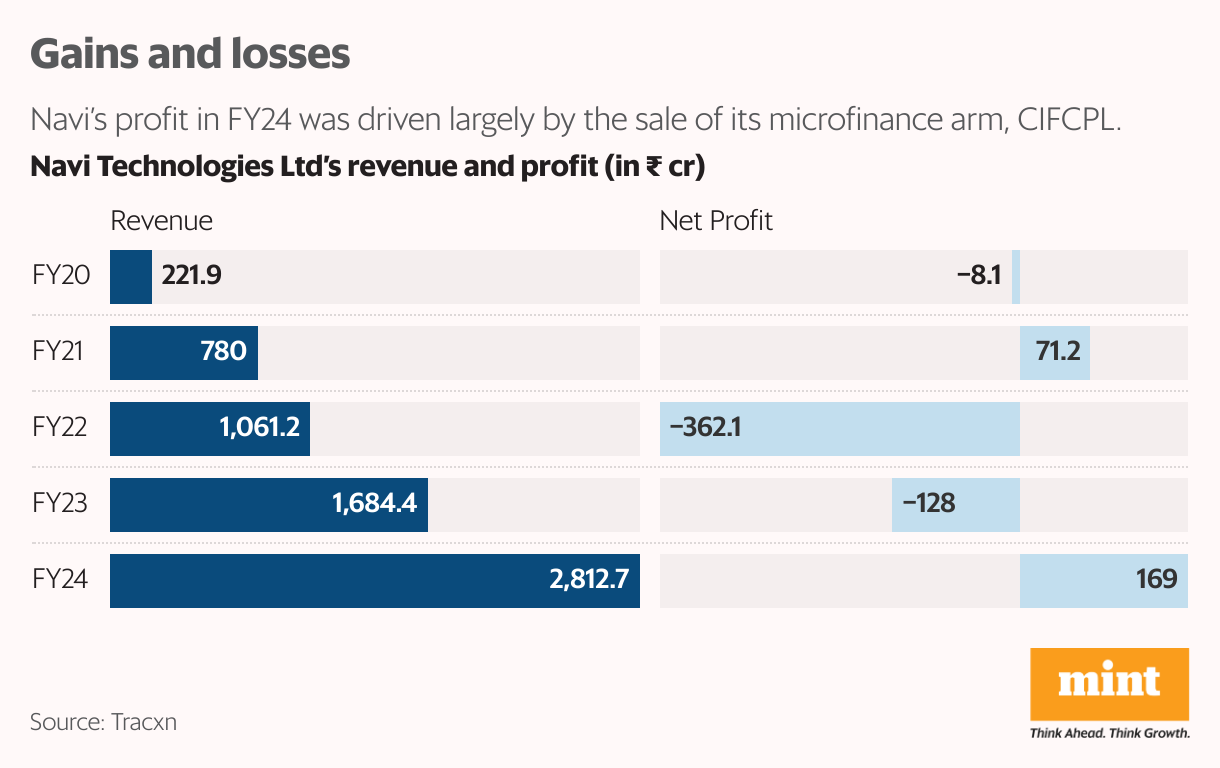

The upheaval has taken a toll on Navi’s financials. After turning profitable in FY21 with ₹71.2 crore in profit, the company slipped back into the red, to report a loss of ₹362.1 crore in FY22 and ₹128 crore in FY23. This was followed by a profit of ₹169 crore in FY24, driven largely by the sale of its microfinance arm CIFCPL, data from Tracxn showed. Excluding the one-time gain, Navi posted a loss of ₹216 crore for that fiscal year, the data showed.

Revenue, however, has grown at an average annual rate of 45%, rising from ₹779.1 crore in FY21 to ₹2,290.7 crore in FY24. But here again, the revenue in FY24 reflects Navi’s earnings after the sale of CIFCPL to Svatantra Microfin.

Spate of exits

Under Navi’s structure—which features various financial entities under one roof—each division functions almost like a mini-startup and has its own head or chief executive officer (CEO). Four such heads or top executives have exited Navi in the past three years to start up on their own. These exits have hit Navi at critical junctures, causing it to limp when Bansal aspired to sprint.

One of the earliest high-profile exits was in March 2022, when Saurabh Jain, CEO of Navi Mutual Fund, left to start Stable Money, a fixed deposit investment platform, when Navi was actively looking at an IPO.

Shobhit Agarwal, who headed Navi’s lending business (personal loans and housing finance), and Apurv Anand, a vice president at the company, quit just last month to launch an asset management company together, Moneycontrol reported. Riya Bhattacharya, former CEO of Navi Finserv, exited in November 2022 after nearly four years with the company to build her own fintech venture, Rio, and offer credit over UPI services.

View Full Image

Industry experts have also questioned Bansal’s approach towards culture building in the company. “A team of almost 50 senior executives were let go abruptly back in 2020 over phone calls. In the following year, the company moved its offices (for the mutual fund subsidiary) almost within days from Mumbai to Bengaluru,” an industry player aware of the developments told Mint. “The abrupt manner in which such decisions were approached have left a bad taste in the mouth for Navi’s workforce.”

Bansal has responded to the ground shifting under his feet. In February, he stepped aside as CEO to become executive chairman, handing over the reins to senior executives while focusing on strategy, AI, and technology. “I have taken myself out of day-to-day operations so that I can focus on these things,” he said. “Whoever gets AI right is going to have a big advantage in this space.”

Deep commitment

After the RBI’s lending ban on Navi Finserv in October 2024, Bansal personally spearheaded a turnaround plan, earning a reversal of the ban in less than 45 days. “After we resumed lending, it took some time to ramp up again. Our loans aren’t long-term—these are two-year loans, not 15-year ones. So, when you pause lending, the book starts running down quickly,” Bansal explained.

According to the Navi founder, revenue growth took a hit as a result of the ban, impacting profitability. He expects the fintech to have ended FY25 close to breakeven and not profitable (the company generally files its financials with the ministry of corporate affairs by October).

“We invested a lot after that (the RBI ban) in tech-driven compliance monitoring systems, which allows us to be much more responsive, in terms of regulatory changes, or any gaps that emerge,” said Bansal.

To shore up funds for Navi, Bansal has been selling personal investments, including his stakes in Ola and Ather Energy.

“Even though unsecured lending is out of favour, Bansal’s approach of overhauling risk policies, tightening compliance, and appointing top auditors shows he is serious about earning back regulator trust,” said an industry expert with direct knowledge of Navi’s internal workings.

Bansal’s commitment certainly runs deep. To shore up funds for Navi, he has been selling personal investments, including his stakes in Ola and Ather Energy.

“Starting Flipkart wasn’t about building a massive, multi-billion dollar company from day one. In fact, around 2009, our first pitch to Accel Partners projected that we could become a $100 million company in 10 years. That was our mindset back then,” said Bansal. Flipkart is aiming to go public in India as soon as next year, with an IPO valuation target of $60 billion to $70 billion.

“You can’t really plan these things in detail,” said Bansal. “What matters is getting into the right space, solving meaningful problems that impact millions of people, and building a business around that. The rest follows.”